State Of Technology: Storage -- The Key Takeaways

Everything Channel's Institute for Partner Education & Development (IPED) surveyed solution providers around the country to get a closer look at the products, services and trends driving the storage market now and into 2009 and beyond.

Overall, VARs surveyed were bullish on sales and profit growth potential for the storage market over the next 12 months. From a 30,000 foot view of the market:

• Managed services are the sweet spot

• Services yield the greatest profits and also have the greatest planned rate of adoption among all storage technologies/services

• Business needs for storage, particularly in disaster recovery, are a key driver of growth

• Small business financing limitations do much to hamper growth

• Hardware still dominates storage sales but services are gaining

In the storage community, the median growth rate among solution providers experiencing greater than 3 percent growth year over year from 2007 to 2008 was 15 percent.

About 29 percent of solution providers surveyed told Everything Channel their profit margins grew compared to the same time in 2007. The majority of solution providers, about 60 percent, indicated that profits remained steady (meaning they went up or down by less than 3 percent), while 11 percent of solution providers reported a decrease in profit margins compared to a year ago.

Solution providers attributed a range of factors to growth in their storage solutions' profit margins, and the most commonly noted factor was attaching more services and other value-add components to sales. Some solution providers indicated that high-end solutions, a better handle on selling costs and an increased emphasis on storage services also contributed to growth.

Solution providers were asked which storage products and technologies drive their bottom lines, and survey respondents indicated hard drives (SATA, SAS, SCSI, Fibre Channel) more than any other, with 63 percent of solution providers naming it among their present offerings. RAID controllers, NAS hardware and Ethernet switches were among the offerings named by about half of solution providers, and flash Drives, tape Drives, disk arrays and optical drives weren't far behind, either. Even the most infrequently mentioned storage technology/product, replication, was still noted by about 30 percent of respondents.

When asked what technology or product they plan to add over the next 12 months, 17 percent of solution providers mentioned hard drives, with combination NAS/SAN appliances, IP storage and continuous data protection not far behind. WAN acceleration, e-mail archiving and NAS hardware were also steady choices.

Responses from solution providers that presently offer storage services organized primarily into three particular types of service: deployment services, managed services and maintenance services. Deployment services had the edge, with 48 percent.

Solution providers who plan to add services in the next 12 months, however, chose decisively in favor of managed services.

SLIDE 8: GRAPHIC: Bar graph from PPT Slide 12

Disaster recovery is the number one reason for storage product and service purchases, according to solution providers, 78 percent of whom named disaster recovery when asked what's driving demand in the storage market. The infrastructure needs of customers, cost efficiency and loss prevention were also regularly cited, each by more than 50 percent of survey respondents.

More than 55 percent of solution providers told Everything Channel that the biggest sales challenge they face is small business customers that don't have the wallet for comprehensive storage solutions. Solution providers also named margin pressure, large enterprises with tightening IT budgets, competition (both from other VARs and vendors) and difficulty expanding customer bases among other obstacles.

The median percentage of overall solution provider revenue from storage solutions, according to solution providers surveyed, was 10 percent. Solution providers in many other horizontal markets derive half of their revenue from services, but in storage, hardware is still king.

While only 14 percent of storage solution providers offer it and only two percent of those not currently offering it plan to add it in the next 12 months, solution providers see content-addressed storage as having the greatest value-add potential. Respondents were asked to rate storage product categories to the degree of their value-add potential on a scale of 1 ("no value add potential") to 7 (extremely high value-add potential). E-mail archiving, database archiving, continuous data protection and WAN acceleration also saw average scores equal to or greater than 5.5

Solution providers were asked which three storage products/technologies or services will generate the fastest growing sales in the next 12 months, and storage managed services took top honors at 23 percent, with e-mail archiving, IP storage and hard drives not far behind.

Managed services was also the top listed category when solution providers were asked what three storage technologies or services would be most profitable for VARs in the next 12 months. Also, while storage deployment was chosen as the most commonly offered service (see slide 7), VARs surveyed named it as the least profitable type of services offering.

Solution providers had a range of responses when asked how their customers were implementing storage software-as-a-service, though the most commonly cited were hybrid models. More than one-third of respondents indicated that of the choices provided they either saw none of the above or found the question not applicable.

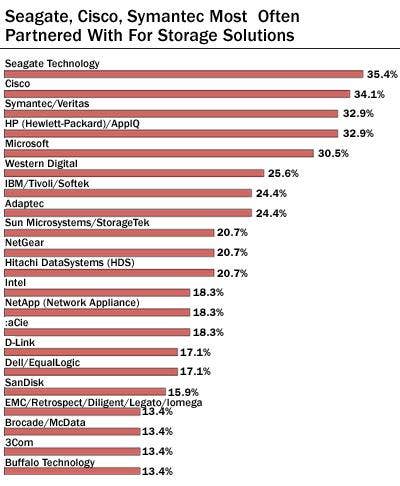

Solution providers were asked which vendors' storage-related hardware or software they resell, recommend, host or service. Seagate and Cisco were the most commonly cited vendors, at more than 35 percent and 34 percent, respectively, and Symantec/Veritas, HP, Microsoft and Western Digital also hovered near the top.

Breaking down greatest growth potential by company-sized market, solution providers weighed in on six different market sizes in five potential growth areas.

"Storage components" include flash drives, hard disk drives, optical drives, RAID controllers and tape drives.

"Storage systems" include disk arrays, fabric-attached storage, IP storage, NAS, SAN, combination SAN/NAS appliances, thin provisioning, tape libraries/autoloaders, virtual tape libraries and external-attached storage.

"Storage infrastructure hardware" includes Fibre Channel Switches, InfiniBand, iSCSI Components, Ethernet switces and WAN acceleration.

"Archiving and content storage software" includes content-addressed storage, database archiving, e-mail archiving and hierarchical/tiered storage management.

"Backup and recovery software" includes continuous data protection, data de-duplication and compression, replication and virtual tape software.

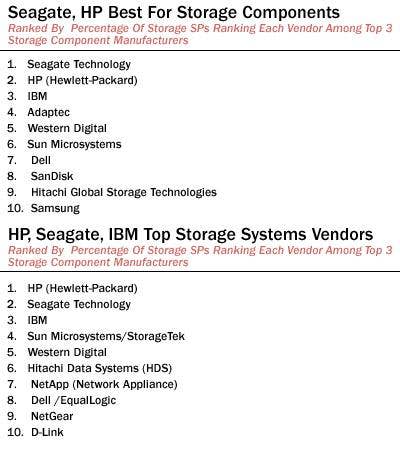

Asked to rank their top three storage component vendors on their ability to deliver the technologies/products needed for solution providers' businesses, solution providers slotted Seagate and HP above all, with IBM, Adaptec and Western Digital rounding out the top 5.

IBM, Western Digital, Seagate and HP were also among the top five noted Storage Systems vendors, with HP taking the top spot and Sun Microsystems/StorageTek coming in number four.

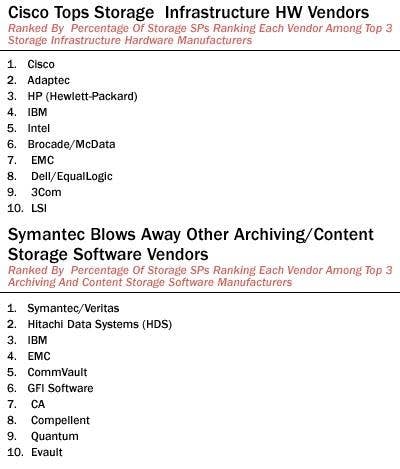

Intel, IBM, HP and Adaptec were all strong in solution providers' estimations for infrastructure hardware vendors, but Cisco was the clear number one overall.

As for archiving/content storage software vendors, Symantec blew away the competition by a country mile, though Hitachi Data Systems, IBM, EMC and CommVault all charted in the top five.

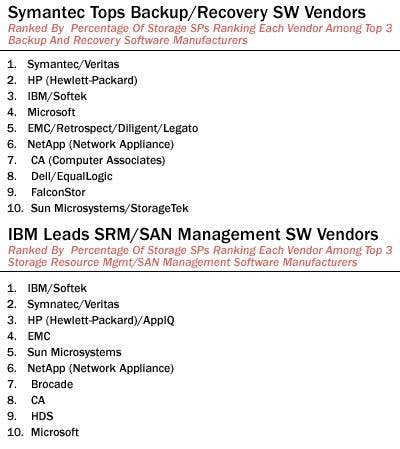

Symantec/Veritas topped solution providers' satisfaction responses in the Backup/Recovery Software category, with HP, IBM/Softek, Microsoft and EMC coming in nos. two through five.

Symantec also had a strong showing in the SRM/SAN Management Software category, but came in number two behind leading vendor IBM/Softek.

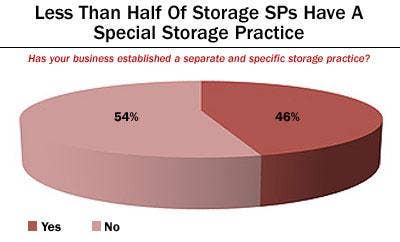

Solution providers were asked whether their business had established a separate and specific storage practice, and results came close to an even-steven split, with just less than half of storage solution providers indicating they had not.