The Bitcoin Saga Continues

Bitcoin Rising

Libertarians love it. Governments hate it. And for mostly the same reasons. The Bitcoin infrastructure transfers digital currency between any two parties without involving financial institutions or government agencies. Transactions are private, encrypted and secure. About 60,000 such transactions happen each day, and they cannot be tracked, traced or taxed. Since the introduction of Bitcoin in 2009, we've witnessed the growth of a bitcoin economy currently worth more $8 billion, dozens of spin-off currencies, and the loss of several exchanges including its largest along with nearly $500 million. We're also seen at least one death, the misidentification of its anonymous inventor and a wild ride for investors. Here are some of the highlights.

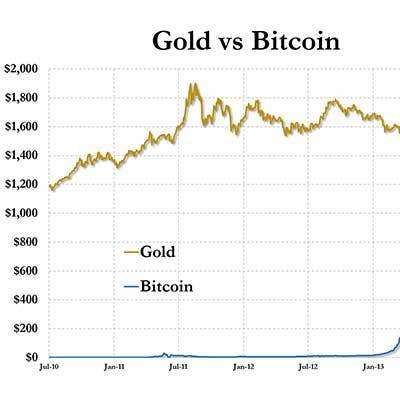

Good as Gold

During its first couple of years, bitcoin went through a series of bubbles and busts, ranging wildly between 30 cents and $32. But during the Cypriot financial crisis of 2012-2013, it shot up over $250, eventually settling at around $50. According to the bitcoin conversion site preev.com, the price of a single bitcoin (BTC) stands at $623. For a brief period in 2013, bitcoins were trading at around $1,250, on par with an ounce of gold at the time.

Mt. Gox Collapse

On Feb. 7, one of the world's largest bitcoin exchanges halted withdrawals of the currency, citing "a bug in the bitcoin software." Tokyo-based Mt. Gox was in trouble; it had apparently misplaced 850,000 bitcoins valued at nearly $475 million. On Feb. 23, CEO Mark Karpeles resigned from the board of the Bitcoin Foundation, on March 9 Mt. Gox filed for bankruptcy protection in the U.S., and on March 12, a U.S. federal judge temporarily froze the assets of Mark Karpeles, former CEO of the exchange (shown). The company also is facing at least one civil suit.

Mistaken Identity?

Meanwhile, a Newsweek reporter was busy trying to identify of the inventor of Bitcoin, who had detailed the plan in an eight-page white paper under the name Satoshi Nakamoto (which in Japan is synonymous with John Smith). In a remarkable coincidence, the Newsweek cover story found an engineer and physicist whose actual name is Dorian Satoshi Nakamoto. Despite his vehement denials, Nakamoto's privacy was destroyed and Newsweek's story has been thoroughly debunked by Jay Caspian Kang.

Media Hounds

Since being "identified" by Newsweek, the press has been relentlessly pursuing Nakamoto. Police 911 call logs list several complaints of reporters hanging around on his porch, knocking on his door with questions and lingering in the street with cameras. As recompense, the bitcoin community donated more than $57,000 (and counting) to help Satoshi cope with the invasion. The ongoing effort was organized by Andreas Antonopoulos, chief security officer for Blockchain.info, a bitcoin service organization based in the U.K.

First Meta CEO Dies

The cryptocurrency saga took a tragic turn when the body of Autumn Radtke, the CEO virtual currency exchange First Meta, was found at the foot of her Singapore apartment building. Though not officially ruled a suicide, her death was widely reported as such. What also remains unclear is whether bitcoin played a role. First Meta is not an exchange for bitcoin, but does accept bitcoins as payment for other virtual currencies. She reportedly took great interest in Bitcoin.

Bitcoin Accepted Here

For tech companies, accepting bitcoin as payment for goods and services can bring much benefit with minimal risk. It's free to accept bitcoin as a merchant and there are no chargebacks or bank fees. There are numerous POS apps, including a free one released by Blockchain.info in mid-March. Bitcoin accounts cannot be frozen, they can be used in every country, and there are no prerequisites or arbitrary spending minimums. What's more, companies accepting bitcoin gain exposure to the bitcoin economy and tend to receive additional business that way.