Data Center M&A On Pace To Break Record In 2019

‘We expect to see a lot more data center M&A over the next five years,’ says John Dinsdale, chief analyst at Synergy Research Group.

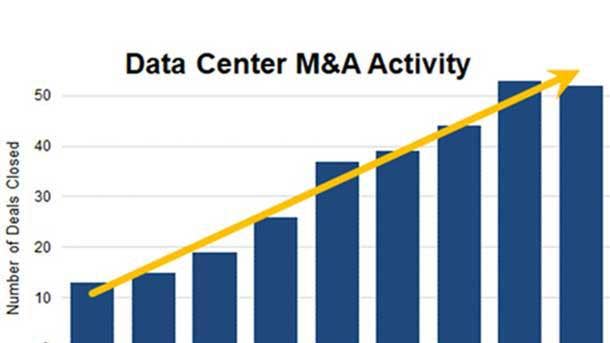

A whopping 52 data center-oriented acquisitions closed in the first half of 2019, up 18 percent year over year, setting up 2019 to become a record year for data center M&A, according to new data from Synergy Research Group.

John Dinsdale, chief analyst at Synergy Research Group, said the spike in data center acquisitions is the result of enterprises shifting workloads to cloud providers or using co-location facilities to house their IT infrastructure.

“Moving IT operations to the cloud can save money, but more importantly it results in more flexibility, faster response to changing needs, and a greater ability to support internal users rather than having to focus on infrastructure,” said Dinsdale in an interview with CRN. “Moving infrastructure to a colocation facility tends to be more about cost saving and freeing up internal resources.”

[Related: Data Center Rising Star eStruxture Buys Shaw Communications’ Calgary Facility]

Dinsdale said as enterprises make this change, more and more data centers are being put up for sale. This leads to colocation providers buying the data centers in an effort to grow their global footprint to better serve both enterprises and cloud providers.

The two companies that continue to lead the M&A charge are Digital Reality and Equinix, which in aggregate account for 36 percent of the value of deals closed over the last four years.

In the first half of 2019, 52 data center acquisitions closed, which exceeded the total amount closed in whole year of 2016. Eight more deals have closed since the beginning of July while 14 more have been agreed upon with formal closure pending.

The three largest deals this year so far were all valued at over $500,000,000, according to Synergy. One was Berkshire Partners acquiring a majority stake in Johannesburg-based Teraco. Africa is a highly under-developed market with Teraco being one of the few established major data center operations in the region.

Another one of the largest acquisitions this year was SUNeVision, owner of data operator iAdvantage, purchasing a data center site in Hong Kong. Hong Kong is a regional hotspot with high demand for a scarce supply of suitable data center buildings or sites, according to Dinsdale. Digital Colony’s acquisition of Peer 1 was another large M&A data center purchase this year.

Since 2015, the largest deals to be closed are the acquisition of DuPont Fabros by Digital Realty, the Equinix acquisition of Verizon’s data centers and Equinix’s acquisition of Telecity. Other notable data center operators who have been strong on the M&A front include CyrusOne, Iron Mountain, Digital Bridge/DataBank, NTT and Carter Validus.

Synergy has identified well over 300 closed data center deals with an aggregate value of over $65 billion since 2015.

“Analysis of data center M&A activity helps to affirm some clear trends in the industry, not least of which is that enterprises increasingly do not want to own or operate their own data centers,” said Dinsdale. “We expect to see a lot more data center M&A over the next five years.”